Succession—There is Still Time

By Ben Hamrick, CPA Many would say that CPA firm succession is one of the most significant issues facing the...

ONLINE CPE REGISTRATION UPDATE

As NCACPA completes its system migration, registration for online CPE courses will temporarily close at 12:00 a.m. on the day prior to each program to allow for accurate attendance and CPE processing. We appreciate your understanding and will share updates once this step is no longer necessary. Please contact Solutions Support at 800-469-1352 with questions.

As accounting services shift and technology integrates into the profession, “CPA” takes on a new meaning. NCACPA’s blog, CPA Today, aims to define what it means to be a CPA in today’s rapidly evolving world. Here you’ll discover articles, spotlights, and blurbs covering a wide range of topics.

The statements and opinions expressed are those of the authors and do not necessarily reflect those of staff, officers, board members, or members.

By Ben Hamrick, CPA Many would say that CPA firm succession is one of the most significant issues facing the...

The U.S. has seen historic levels of federal funding in response to the COVID-19 pandemic. Various laws, including the CARES...

This week’s podcast focuses on the following items: A quick discussion of what know (little) and don’t know (a lot)...

By Sandra Finerghty, Supporting Strategies What is the future of remote work? Many businesses weren’t ready when COVID-19 forced them...

Click READ THE ARTICLE below to view the full news post!

Source: Accounting Today

Thomas G. Stephens, Jr., CPA, CITP, CGMA Collaboration is more important today than it ever has been. With many team...

By Randy Johnston and Sam Saab Higher client expectations and economic demands are causing firms of all sizes to re-evaluate...

Click READ THE ARTICLE below to view the full blog post!

Source: Accounting Today

Source: Accounting Today

By the Student Outreach, Advancement, and Recruitment (SOAR) Committee The world as we know it has changed. The impacts of...

Tax season is when millions of people and organizations turn to the expertise of professionals such as tax preparers, tax...

Women’s Equality Day, celebrated annually on August 26, marks the anniversary of the ratification of the 19th Amendment which granted...

The home office deduction allows qualifying taxpayers to deduct certain home expenses on their tax return. With more people working...

For most homeowners, their mortgage is their biggest monthly expense. But job losses around the country are hammering people’s finances,...

By Ken Tysiac The racial injustice taking place throughout the United States has hit home hard for members of the...

Following NCACPA’s Annual Business Meeting and Focus on the Profession session, we were delighted by the influx of positive input...

By Laura Morgan Roberts and Ella F. Washington The United States is in crisis. As we write this article, videos of racial...

By Donald J. Kaiser, CPA, McCarthy & Company, PC Internal controls are among the most important anti-fraud controls that...

This week’s podcast focuses on the following items: IRS changes its guidance on the payment of health insurance only and...

This week’s podcast focuses on the following items: PPP loan updates on corporate groups, businesses sold after February 15, 2020,...

By Will Douglas Heaven Far from breaking it, the surge in usage the internet is seeing right now is driving...

This week’s podcast focuses on the following items: PPP Loan program and EIDL Grants Get Additional Funding PPP guidance raises...

This week’s podcast focuses on the following items: SBA issues guidance on self-employed taxpayers and partners for PPP loan program...

This week’s podcast focuses on the following items: Recovery Rebate for Individuals, Including Advance Payment Deferral of the Required Minimum...

This week’s podcast focuses on the following items: Payroll tax credit starts on April 1. IRS reverses courses, announces gift/GSTT...

Maintaining a social media account can feel like a second job to some, while others utilize it as a...

This week’s podcast focuses on the following items: Congress passes payroll tax credit for newly mandated paid sick leave Initial...

This week’s podcast focuses on the following items: President declares emergency over COVID-19, directs Treasury to provide relief–and now we...

Becoming a student member of your state society is an excellent idea, and there are a whole lot of reasons to...

This week’s podcast focuses on the following items: IRS denies a taxpayer’s request to make a late mark to market...

By Stephanie Vozza Looking for a new job is stressful enough, but to make matters more challenging, some interview questions...

This week’s podcast focuses on the following items: Taxpayer who voluntarily exited OVDI program ended up with very poor result....

This week’s podcast focuses on the following items: Proposed regulations can be relied upon in the interim, as well as...

By Ranica Arrowsmith This year’s top products were selected for their contact with innovation, whether it’s in actual technology—injecting artificial intelligence,...

This week’s podcast focuses on the following items: Regulations implementing changes to FAVR and cents-per-mile methods finalized by IRS OIRA...

By Sandra Finerghty, Supporting Strategies Even the most competent, upstanding, conscientious business owners tend to fret over filing their taxes....

This week’s podcast focuses on the following items: Special agent in charge of Los Angeles CID talks about their potential...

By Brooks Aker, CPA The Young CPA Cabinet (“YCPA Cabinet” or “cabinet”) enjoyed terrific accommodations at East Carolina University (ECU)...

By Ben Hamrick, CPA After the (literal) blood, sweat, and tears owners put into a firm, it can be hard...

By Stacee Rash, CPA Retiring partners are not the only CPAs with succession planning on their minds these days. Young...

By Terrence Putney, CPA and Joel Sinkin The end of your professional career is something you will eventually face. How...

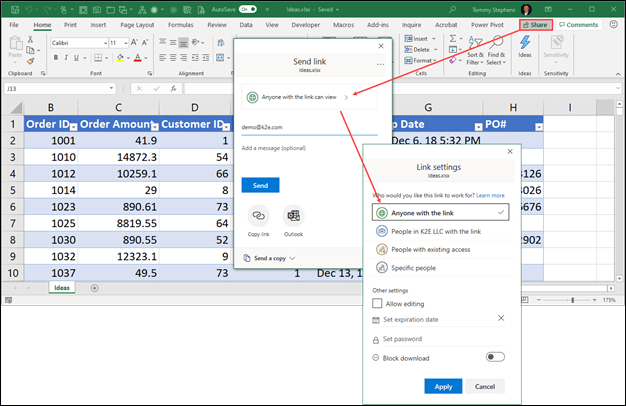

By Randy Johnston, Executive Vice President, K2 Enterprises Are you doing things the same old way? Do you wish there...

$20.20 doesn’t seem like much money. It can get you four lattes from Starbucks, lunch for you and a coworker,...

At NCACPA, we often say that advocacy is a member benefit North Carolina CPAs won’t receive anywhere else, and it’s...

While fraud can damage any organization, it can devastate small businesses, which often lack the resources for proper anti-fraud...

State lawmakers are hopeful that they can reach an agreement on budget adjustments by June 17. The House and Senate...

2020 was tough. COVID-19 made firms of all sizes put their heads down and focus on the rapidly evolving situation...