By Susan S. Coffey, CPA, CGMA, EVP — Public Practice, Association of International Certified Professional Accountants

It’s that time of year when everyone reflects on the past and looks forward to a positive future with personal and professional planning, and new and fresh ideas. You may have some New Year’s resolutions you’d like to accomplish. I have two: From a personal perspective, I’ll look at my financial and personal health. From a professional perspective, I’ll look at planning and execution around securing the future and value of the profession. On the latter, I’m working on a number of initiatives to advance the value of the profession, including the development of technology-based tools to enhance the efficiency, quality and value of audits. Many of you are already starting busy season and are focused on getting through a mountain of work over the next few months.

Whether we’re plotting our 2020 goals or just focusing on getting to March 30 or April 15, we need to think long term. How do we ensure that the future of our profession is bright and that the CPA maintains its strength and relevance for decades to come?

To position ourselves for continued success in a constantly evolving business environment, we must take the necessary steps now.

Evolving CPA licensure

You may have read my blog posts in January, May and July of last year about CPA Evolution, a joint initiative of the National Association of State Boards of Accountancy (NASBA) and the AICPA®. CPA Evolution aims to transform the CPA licensure model to recognize the rapidly changing skills and competencies accountancy requires today and will require in the future.

In summer 2019, NASBA and AICPA leadership developed five guiding principles for a new CPA licensure model, and we asked for your feedback. We heard input from more than 2,000 stakeholders across the profession, including CPAs working in firms of all sizes, CPAs working in business and industry, state CPA societies, academia, state boards of accountancy, accounting students, technology experts and more. Thank you to everyone who shared feedback; your insights helped us determine a viable path forward.

What we heard from you

There were a few common themes that emerged from your feedback:

- By far the No. 1 comment we heard was support for the need to change CPA licensure. You also told us there should be a greater emphasis on technology skills and knowledge taught in university and tested on the CPA Exam.

- You said that any new licensure model should require all CPAs to demonstrate strong common core competencies in accounting, auditing, tax and technology.

- You asked questions about the specifics of implementing a new CPA licensure model, such as what would be considered “core” common knowledge, how the education requirements might change and how licensure could evolve in the current state legislative environment.

Although CPA Evolution originally started because of the impact of technology on the profession, we heard an overarching theme from you that we also need to consider other disrupting factors.

For example, we heard that newly licensed CPAs need to know more than ever before. The CPA profession’s body of knowledge is growing rapidly as the number of accounting and auditing standards have quadrupled and quintupled, respectively, since 1980. The Internal Revenue Code is also larger and more complex. With firms automating or sending offshore many procedures that newly licensed CPAs used to perform, entry-level CPAs are doing work traditionally assigned to more experienced CPAs.

CPA licensure needs to evolve to address this challenge… so how?

NASBA and the AICPA’s proposed CPA licensure model

After reviewing all the feedback, conducting additional research and considering multiple possibilities for evolving licensure, NASBA and AICPA leadership developed a draft licensure model that we believe best positions our profession for the future.

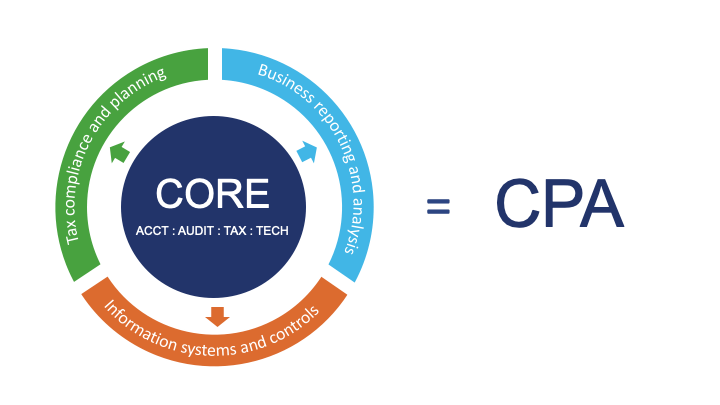

NASBA and AICPA leadership recommend that we move to a core + discipline CPA licensure model. Here’s how it might work:

- Each CPA candidate would be required to complete the same robust core education and examination in accounting, auditing, tax and technology — the navy “core.”

- Each candidate would also choose a discipline in which to demonstrate deeper knowledge. The three potential disciplines we’ve initially identified reflect three pillars of the profession:

- Business reporting and analysis

- Information systems and controls

- Tax compliance and planning

- Every successful candidate — regardless of their chosen discipline — would receive a CPA license with the same rights and privileges licensed CPAs have today. We knew this was important to you — that all CPAs share a common core of knowledge and the same CPA license.

This model is responsive to the feedback we heard, as it would build accounting, auditing, tax and technology knowledge into one robust common core. We also believe a core + discipline licensure model reflects the realities of practice by requiring deeper knowledge in one of three areas of practice that are key to the profession.

This licensure approach also builds flexibility into our model, allowing us to adapt and grow over time. This will help future-proof the CPA for years as the profession continues to evolve. But the model would still result in one CPA license, keeping the profession strong and not splintering the credential.

Ultimately, this licensure approach would enhance public protection, as it would produce candidates who have the deep knowledge necessary to meet the needs of organizations and perform high-quality work.

What a core + discipline model could look like

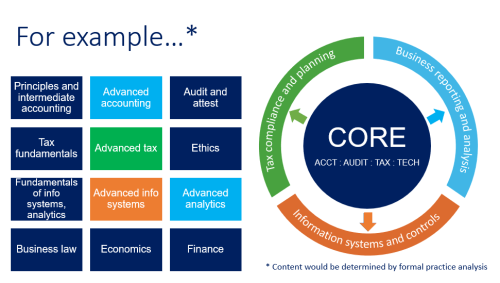

One of the most common pieces of feedback we received was that “the devil is in the details” with this project. People asked what would be considered “core” vs. “discipline” knowledge.

Ultimately, the exact content of the core vs. the disciplines would be determined through revisions to state board education and licensure requirements followed by a CPA Exam practice analysis. As a part of its ongoing efforts to maintain the validity and reliability of the Exam, the AICPA (with oversight by the Board of Examiners) conducts periodic practice analyses to gather information about the state of the profession and the work of newly licensed CPAs. These research initiatives inform potential changes and updates to the CPA Exam and maintain its alignment with professional practice. You can learn more about the CPA Exam Practice Analyses here.

However, while the specific content of the core vs. the disciplines has not been determined, the below graphic gives you some insight into NASBA and the AICPA’s current thinking about where topics could fall. The topics below are color-coordinated with either the core or a discipline. This is not an exhaustive list, but it gives some indication into what we’re thinking.

For example, we could envision that advanced accounting topics such as business combinations, derivatives and foreign currency translations would move to the business reporting and analysis discipline. Advanced tax topics, such as AMT and estate and gifts tax, could move to tax compliance and planning. Advanced information systems topics, such as cybersecurity and information security and privacy, could move to the information systems and controls discipline.

Again, this division of content is not final, and a CPA Exam practice analysis would determine the exact content of the core vs. disciplines. Hopefully, it provides some clarity into our thought process.

What’s next

CPA Evolution is still a work in progress. Over the next few months, we’ll gather more feedback on this proposed licensure model from stakeholders across the profession and, particularly, state boards of accountancy. Our goal is to finalize a new approach to CPA licensure acceptable to the state boards by this summer.

Once we have a final approach, we’ll collaborate with NASBA, state CPA societies and state boards of accountancy to establish a multi-year implementation plan.

Visit our website to learn more information about the CPA Evolution initiative and our proposed licensure model. You can also watch Carl Mayes, CPA, the AICPA’s Associate Director — CPA Quality & Evolution, discuss the proposed model in more detail in the below video.

If you’d like to share your thoughts on the proposed model, we welcome your feedback. Please email [email protected].

As we start the 2020s this year, let’s not forget to think ahead to the next decade and beyond. I’m excited to take this step, and proud of our profession’s commitment to keep the CPA strong for years to come.

Originally published by the AICPA.