By: Scott Showalter

Did you know NCACPA has vision and mission statements to guide its future direction? I didn’t either, until I became a member of the Board of Directors. The vision and mission statements were last updated in 2006. I think it’s safe to assume we’re all in agreement that things look slightly different now than they did thirteen years ago.

As part of NCACPA’s centennial celebration, the Board is having a lot of fun reminiscing on the past 100 years. We are also engaging in conversations about how to ensure the future success of this organization while navigating the great pace of change happening all around us. At the 2019 Leadership Summit in May, Chair of the Board Austin Wachter challenged the Association’s leadership to imagine what NCACPA would look like in 100 years. These discussions started to get the ball rolling, and led to great conversations about the landscape of the accounting profession.

SO…WHY NOW?

If I were to answer the question of why the Board decided to study these statements in a single word, it would be—change. In fact, Austin was surprised to learn that it had been over a decade since the vision and mission statements had been reviewed. He said, “Given the rapidly changing environment for our profession, and the length of time since we last revisited these statements, this was a perfect opportunity to take a fresh look.” Not only have there been many changes in the accounting profession since 2006 (when the statements were revised), but more importantly, I ask you to consider the changes currently facing the accounting profession and the changes projected over the next three to five years. For example:

- Given the pace of change, accounting professionals in public accounting, industry, and government will need to retool their skills.

- Accounting firms and companies have modified their hiring to include individuals who have computer science and data analytics degrees.

- Professionals today are not attracted to joining organizations, but rather would like to purchase needed services without belonging to the organization.

- The lines are blurring between what CPAs and non-CPAs do.

Who will professionals and related organizations in the accounting profession turn to in helping them respond to these changes? Wanting the answer to be NCACPA, we as a board recognized our need to address our statements and determine whether they provided a platform for growth and encouraged future accounting professionals to purchase services from the Association.

A TASK FORCE IS BORN

[column_set id=”1″]

CREATING A COMMON DEFINITION

It was important for the task force to level-set in terms of the definition of vision and mission statements. Vision and mission statements are integral components of an organization’s strategy. The statements are complementary, but unique. They provide the foundation for the strategic initiatives.

THE TASK FORCE’S PROCESS

[column_set id=”2″]

VISION STATEMENT EXPLAINED

Remembering a vision statement is aspirational, forward-looking, and the end state the Association is striving to achieve, the Board unanimously approved the following vision statement:

[column_set id=”3″]A highly valued accounting profession advancing the success of individuals and organizations.

advancing the success – The task force decided the vision should portray the accounting profession as proactive in contributing to the success of individuals, organizations, and the community served by the accounting profession. Recognizing success can have numerous meanings, it is appropriate for success for be determined in context of who is being served.

of individuals and organizations – When it comes to who is served by the accounting profession, it was determined best to use the phrase “individuals and organizations.” That includes the individuals and organizations within the accounting profession as well as the individuals, organization, and the community served by the accounting profession.

MISSION STATEMENT EXPLAINED

Remembering a mission statement describes what an organization does and who it does it for, the Board unanimously approved the following mission statement:

[column_set id=”4″] [column_set id=”5″]Enhancing the accounting profession and the community it serves through advocacy, connections, education, and resources.

One question we received at the Board meeting concerned the listing order of these four areas. Was it in order of priority? The answer is no. The task force decided to list the areas in alphabetical order because the priority of each area will change over time and the mission should not be adjusted as the priority of each area changes.

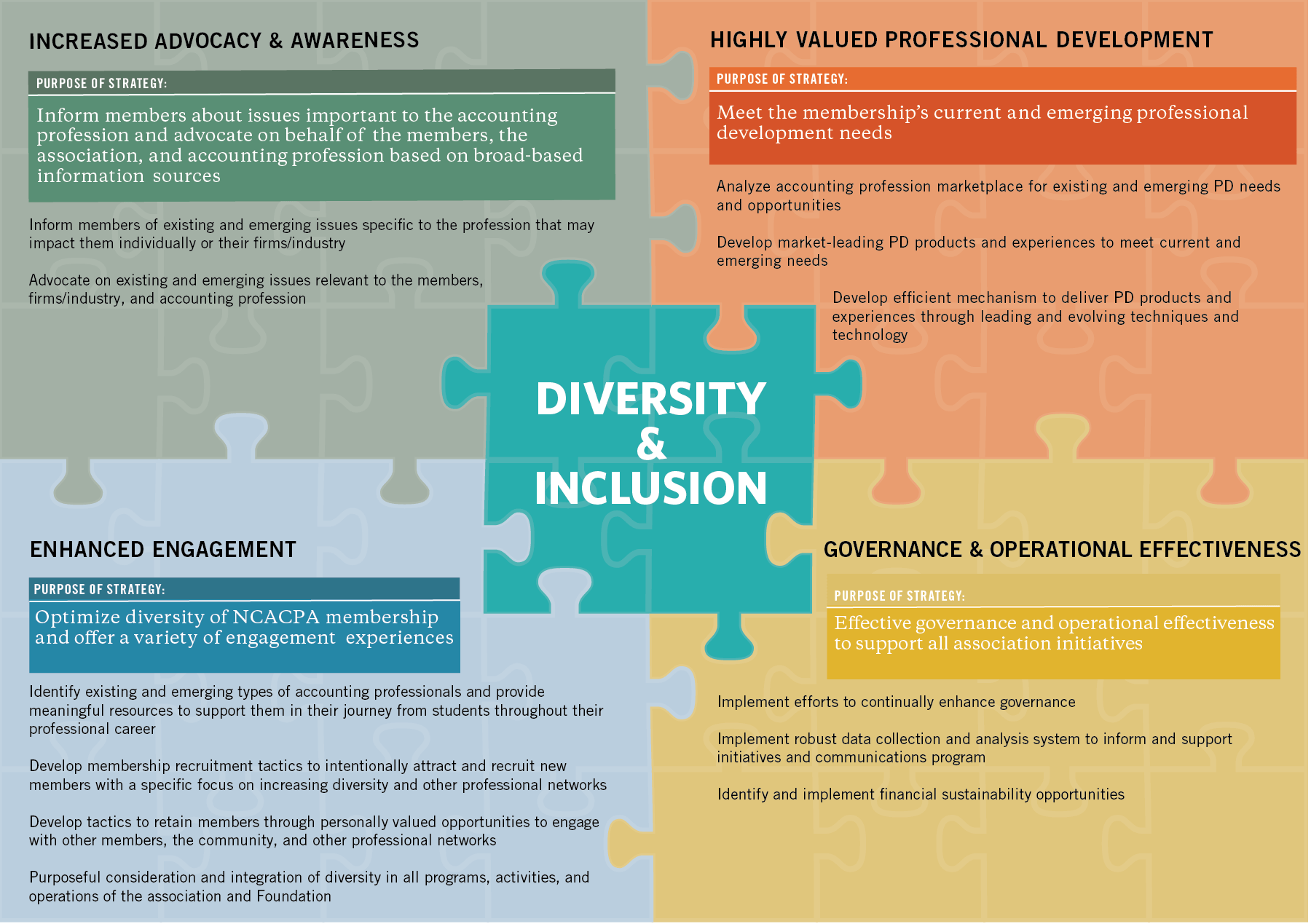

For those of you familiar with the Association’s strategic initiatives, you will see some similarities. Although not a requirement of the assessment effort, the good news is the current interlocking strategic initiatives fit well with the enhanced vision and mission statements.

COMPARISON TO PREVIOUS STATEMENTS

Below is a comparison of the previous and enhanced statements:

[column_set id=”6″]The biggest difference is that the previous statement is focused on the Association and limited to the state of North Carolina. As previously explained, a vision statement should focus on the future state the Association seeks to achieve, so the enhanced vision statement focuses on the future of the accounting profession and does not limit the Association’s influence to North Carolina. The Board foresees near-term and longer-term opportunities to offer services to individuals and organizations outside of North Carolina, and the enhanced vision recognizes this potential.

[column_set id=”7″]The task force concluded use of the word “enhancing” was more proactive than using “promotes.” Further, use of advocacy, connections, education, and resources clearly states what the Association can provide today and tomorrow, while “competence, integrity, and civic responsibility” were more of an outcome than a service. Again, the previous mission limited the Association to North Carolina, while the enhanced statement expands influence beyond our state.

SUMMARY

My fervent hope is that given the explanations offered, you can understand why the Board undertook this effort and appreciate the task force’s work in creating change. After hearing the task force’s recommendation, Chair Austin Wachter said, “I’m confident these new statements will serve as an important guide for NCACPA as we enter our second century.” This is a sound point because with these enhanced statements, NCACPA is better positioned to meet the needs of an ever-changing accounting profession and openly communicate the role the North Carolina Association of Certified Public Accountants plays in providing for them and the community they serve.

As mentioned, the Board requested a robust communications plan to inform the membership. While this article is the first effort, many others will follow in December. The NCACPA team is developing a webcast of the presentation that the Board received, content for e-newsletters and the website, and more. Members of the task force will also share information via Connect in December.

[column_set id=”8″]